Developing the Annual Budget

The development of Jupiter Bay's Annual Budget is a tedious and complex process requiring the use of interrelated spreadsheets that analyze current year expenditures, predict probable cost increases, and calculate revenues and fees needed to fund projected expenses.

The development of Jupiter Bay's Annual Budget is a tedious and complex process requiring the use of interrelated spreadsheets that analyze current year expenditures, predict probable cost increases, and calculate revenues and fees needed to fund projected expenses.

The development of Jupiter Bay's Annual Budget is a tedious and complex process requiring the use of interrelated spreadsheets that analyze current year expenditures, predict probable cost increases, and calculate revenues and fees needed to fund projected expenses.

The development of Jupiter Bay's Annual Budget is a tedious and complex process requiring the use of interrelated spreadsheets that analyze current year expenditures, predict probable cost increases, and calculate revenues and fees needed to fund projected expenses.Automating the Budget Process

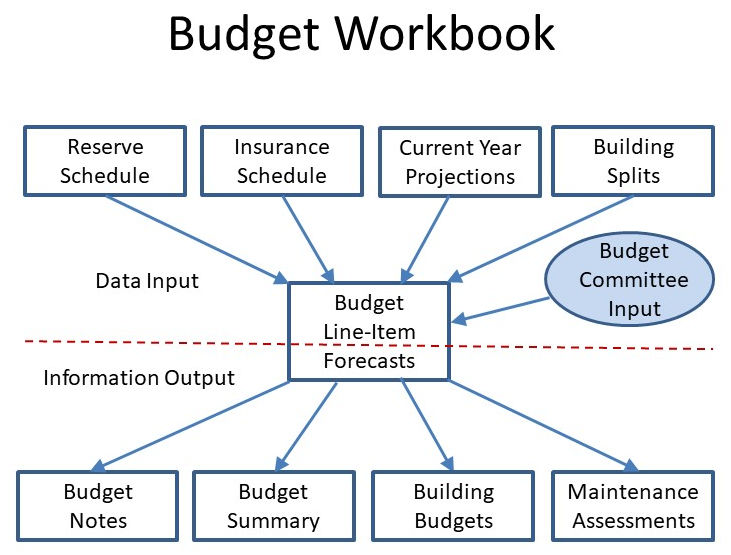

Preparation of the Annual Budget can be simplified, with changes reflected instantly, through use of a series of interlinked Excel spreadsheets. This process uses historical known information, such as the reserve schedule, data collected from insurance vendors, and 9 months of current-year expenses and combines it with Budget Committee input to produce all of the spreadsheets for the next year's budget. Quarterly Assessments are calculated automatically as a byproduct of the budgeting process, allowing various "what-if" line-item change scenarios.

The Budget Committee uses comparison data, provided by the Budget Workbook, for each line item showing last year's budget figure and current year expense projection to enable them to see and respond to changes and trends.

Budget Process -- (B) Reserve Expense

11. The other section of the budget is the reserve section. The reserve section contains funds that are set aside (restricted) for specific expenditures that will be incurred in the future. Usually, such expenditures relate to the cost of major repairs to, or replacements of, the condominium property. If money is not set aside for these expenses, unit owners will usually have to pay a special assessment at the time such repair or replacement occurs. Please reference the "Reserves Page" of this website for comprehensive information on reserves.

- The Condominium Act requires that reserves be established for certain items including: roof replacement, building painting, pavement resurfacing and any other item of capital expenditure or deferred maintenance that exceeds $25,000. Jupiter Bay has established additional reserves (see below) for other community and building capital expenditures and deferred maintenance. Deferred maintenance means any maintenance or repair that will be performed less frequently than yearly and will result in maintaining the useful life of an asset.

12. Jupiter Bay maintains the following Community Common-Area reserve accounts: Restoration (bridge, lake and waterfall), East & West Pools, Irrigation, Paving, and Common Buildings (pool, maintenance shed & pump house).

13. Jupiter Bay maintains the following Building-Related reserve accounts: Building Restoration, Elevators, Building Painting, Roof Replacement, and Generator & Booster Pumps (East only). The structural integrity reserve study (SIRS) added plumbing, electrical, and exterior doors and fixtures accounts.

14. Determine Replacement Cost and Years of Life for each reserve item (both common reserves and reserves for each individual association/building):

- Replacement Cost is determined by actual prior expenditures (with an inflation adjustment) or current vendor quotes. Once established, the Replacement Cost may increase slightly due to inflation but would not change substantially from year to year.

- Years of Life is determined by historical experience, vendor input and from experiences of other similar associations. The following Years of Life values are commonly used: Paint (5-7 yr.), Roof (12-20 yr.), Elevator (20-25 yr.), Spalling (12-18 yr.), Pools (10-15 yr.), and Paving (18-22 yr.).

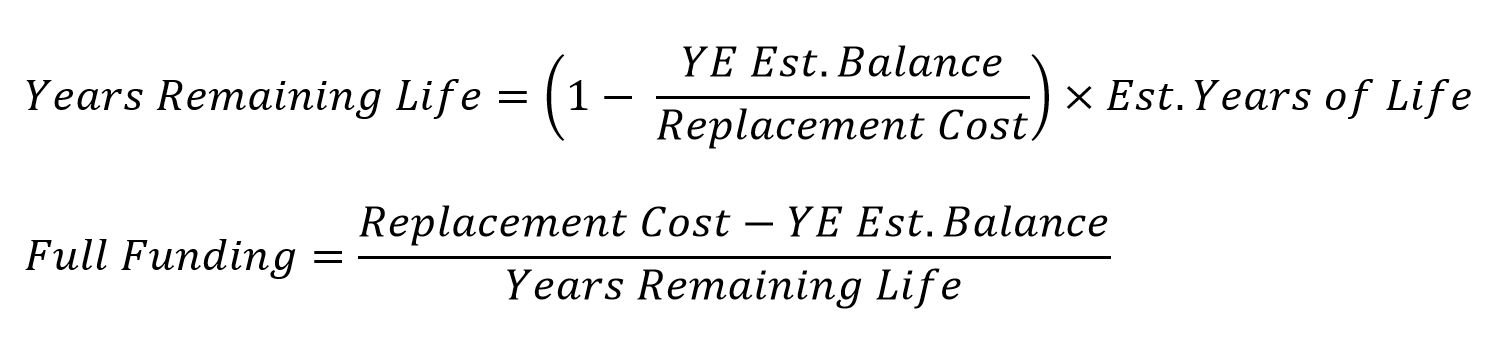

15. Years Remaining Life and Full Funding of reserves for the new year are calculated mathematically to reflect the requirements to reach full replacement cost based on current balance:

Following is a sample Reserve Schedule, using the formulas above, for the Association’s Common Areas:

| Reserve Fund | Prior Yearend Balance | Replacement Cost | Years Of Life | Years Left (Calc.) | Full Funding Contr. |

| Restoration - Bridge, Lake, Tennis, Bocce | 7,395 | 109,374 | 6 | 6 | 18,229 |

| East & West Pools - Resurface, Deck, Furniture | 58,646 | 162,216 | 10 | 6 | 16,222 |

| Irrigation | 14,060 | 32,828 | 8 | 5 | 4,104 |

| Paving | 184,814 | 770,461 | 22 | 17 | 35,021 |

| Common Buildings | 8,765 | 105,621 | 18 | 15 | 6,457 |

| Totals | 273,680 | 1,180,500 | 80,033 |

16. If a reserve fund balance is negative, the total amount necessary to bring a negative account balance to zero must be added to the Full Funding calculation.

17. Allocate Common Reserve funding expenses to each association – 37.602% (135/359) to the East and 8.914% (32/359) to the other 7 associations.